Artificial Intelligence, Real Speculation

How is AI financed?

- Venture Capital and Valuations

Artificial intelligence (“AI”) companies have raised more $190 billion in venture capital in 2025 alone, according to research published by Pitchbook, with most of the funding allocated to more established businesses like OpenAI, Anthropic, and xAi. As a result, valuations have been driven sky high, with promises of substantial future capital commitments.

More than half of all venture capital investments in 2025 were allocated toward AI, according to the same Pitchbook research. But valuations are just one piece of the puzzle.

Venture capital valuation relies on a multiple of the capital invested. It is not a fundamental measure of the businesses worth. There are also no meaningful comparables in the methodology.

If it was just equity pouring into the sector, the potential future stress may not be so painful. But AI has capacity to expand beyond just the sector, given there is a lot of debt in the system backed by AI and related businesses.

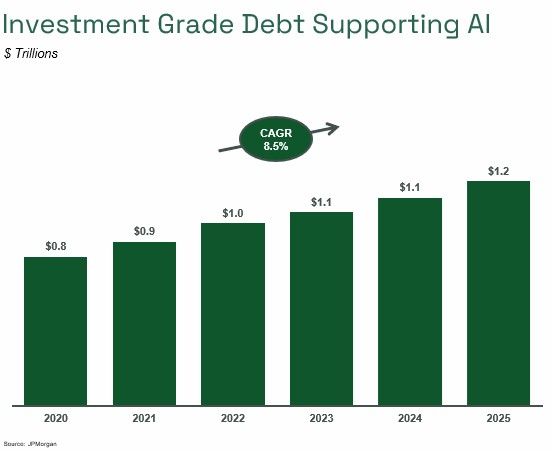

Investment Grade Debt and Valuations

According to JPMorgan research, investment grade AI related debt now accounts for more than 14% of total investment grade issuances, from companies including Oracle, Apple, and others.

Given the strength of these high grade issuers, we would expect less risk on repayment, but looking forward, JPMorgan further estimates that the sector will need $1.5 trillion in new investment-grade issuances over the next five years. This amount of principal is likely to fluctuate more closely with valuations of major AI companies like OpenAI, xAI, and Anthropic. Any pullback in valuations would likely slow AI’s expansion or reduce the amount of future debt.

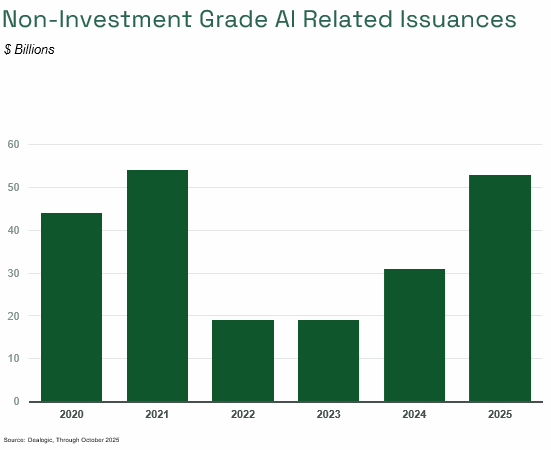

Non-investment Grade Debt

Further down the capital stack, there is non-investment grade debt connected to AI. This debt is harder to measure, but data from Dealogic indicates that there has been increased appetite for this type of debt in 2025 after a quiet period in 2023 and 2024.

The terms related to this debt are not as clear as the investment grade issuances, but the uptick in 2025 across both investment grade and speculative grade is likely due to general market enthusiasm for the sector, and favorable political conditions in technology and AI.

Data Centers, Chips, and Capital Equipment

Whether it be investment grade or not, much of this debt is allocated to Data Center development, along with chips and related capital equipment. Data centers have significant depreciable assets, and so to service this debt and make ongoing maintenance capex, they will need to monetize reasonably quickly. That monetization is one of the larger unanswered questions around large language models (“LLMs”) and how all this investment can be captured. Time will tell if demand exists, but for now, we can remain calm knowing that credit spreads are generally low in the market, and among AI investment grade AI issuances, suggesting lower credit risks in the market.

Circular Vendor Financing

There is also a significant amount of vendor financing in the AI space. Apart from investment capital, the business of chips is also driving AI investment. Companies like Nvidia and AMD leverage both their scale to invest in AI research companies like OpenAI, who then use that investment to purchase chips from companies like Nvidia. This has been referenced as the infamous “circular financing” scheme, which increases risks by concentrating capital. It may also be a signal that there isn’t enough capital available in the economy to fund from other sources just yet (or at least affordable capital).

How does AI Plan to Make Money

Selling tokens, subscriptions, and licenses is the current plan.

First, AI research companies like xAI, Anthropic, and OpenAI sell tokens that are used when querying AI models. Second, they charge subscriptions to consumers and businesses who use their AI and agentic models. Third, they generate revenue through licensing agreements with technology partners, sometimes called hyperscalers, like Microsoft, Amazon’s AWS, Oracle, and Google Cloud. These larger tech companies, many of which are the same investment grade debt issuers, pay fees to these AI research companies for access to their models, which they can then pass on to their cloud customers.

None of these AI research companies makes a profit today, according to media reports as of October 31, 2025. Open AI has ambitious revenue targets, indicating it is on pace to generate $20 billion in revenue in 2025, and hundreds of billions by 2030. OpenAI will need that revenue by 2030 to comply with its $1.4 trillion in Data Center infrastructure deals that it has completed in 2025. Anthropic is optimistic, but less sanguine than OpenAI, targeting $70 billion in revenue by 2028 and to be cash flow positive. xAI is considerably smaller, with an EBITDA target of $2.7 billion by 2027.

Outside of the three headline names conducting AI research and building AI models, there are myriad businesses making investments in AI to support existing functionality, with the expectation that customers will pay for tailored services such as loan servicing, code and script writing, healthcare administration, and countless other applications. These more niche businesses are likely to remain reliant on the availability and affordability of access to AI models like OpenAI’s or Anthropic’s, as well as a reasonable value proposition to their customers.

What about data centers?

Data Centers and the handful of industries agglomerated around Data Centers, are the most direct users impacting commercial real estate in the AI race. They function as large warehouses that lease compute (aka virtual real estate) to companies that need significant processing power.

In the commercial real estate industry, these Data Center operators function a lot like coworking companies. They lease space to users, typically companies like Meta, Amazon, Google, and other enterprise scale companies.

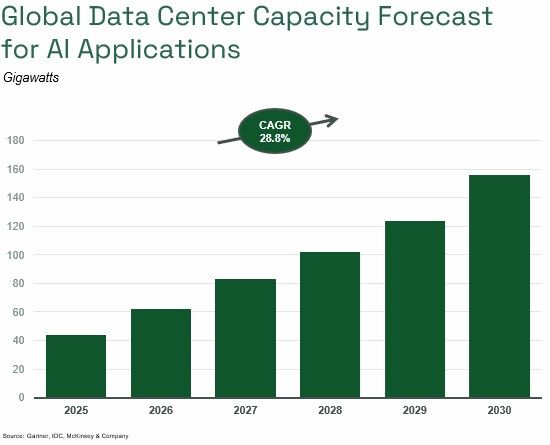

Data Center Growth is expected to increase approximately 350% between 2025 and 2030 according to estimates from McKinsey & Company compiled from market research companies IDC and Gartner.

Demand is often measured in the amount of energy needed to power Data Centers. Data Centers currently require an estimated 44 gigawatts and is forecast to grow to 156 gigawatts by 2030. This type of energy demand might require as much as $1 trillion more in investment over the next five years. If Data Center supply exceeds AI demand, the imbalance could create a period of stagnant growth for AI native companies like OpenAI, Anthropic, and xAI and reduce demand for office and Data Center assets for CRE owners.

Closing Thoughts

AI is unique from previous tech because the creation of LLMs and AI models sits at the intersection of technology and engineering, a niche for which there are few specialists. Additionally, the pool of investors who understand rhythms of both debt and equity investors is quite small. And finally, we have the fact that these businesses are not yet profitable. For these reasons, AI’s credit is still speculative.

AI valuations have become dizzyingly high, with Nvidia’s market capitalization crossing $5 trillion recently, and OpenAI’s private valuation pegged at $500 billion, leaving investors to rely on a handful of technology experts to validate their claims. The lofty valuations give the companies flexibility to tap into the creative financing solutions outlined earlier. If these valuations take a meaningful hit in the next 12 to 18 months, the investment commitments made by companies like OpenAI are likely to miss their mark, and investors in that infrastructure could be poised to assume some credit losses.

Broader macro forces, like capital market liquidity and macro growth, could also disrupt AI’s rapid ascent. We’ve already seen signs of short-term liquidity strained in the overnight repo facilities maintained by the U.S. Federal Reserve. With GDP growth increasingly reliant on AI investment in the U.S., and a softening labor market that could further strain market liquidity, the foundation of AI’s ascent seems less stable than in January of this year.

AI model developers are inherently speculative, as they cannot yet stand on two feet and fund their businesses. Instead, like many VC backed companies that have tread the same dirt, they are reliant on outside capital to fund their businesses.

Commercial real estate professionals across the capital stack should be cautious of extending too large a hand to these companies without doing their proper due diligence. AI companies are taking large leases, including Sierra’s 300 thousand square foot space and OpenAI’s 315 thousand square foot lease, which are both in San Francisco. Similar caution should be exercised with Data Center leases, with companies like CoreWeave operating Data Centers that require significant investment, including debt, which hampers financial flexibility. Understanding legal entity structure, bankruptcy remoteness, and the flow of capital related to individual Data Centers are all necessities for commercial real estate investors and operators.

We believe there is a lot to be excited about with AI, but at a fundamental level, the AI business model remains in its early stages, lacking long-term, standalone sustainability today. The complex symphony of stakeholders in the industry and their ability to access needed capital could also pose as roadblocks to growth (or harbingers of trouble), so cautious optimism seems appropriate for the commercial real estate industry at this time.