AMC Entertainment – Liability Management that’s as Entertaining as a Summer Blockbuster

April 2026

With so much going on in the world these days, it would be nice to curl up with a bucket of popcorn and a good movie. At AMC Entertainment theaters, that is becoming harder to do. This TRA Insight explores what is happening with AMC and what it may portend for owners of retail and hospitality assets where AMC is a tenant.

AMC Entertainment Holdings, Inc.

AMC Entertainment Holdings, Inc. (“AMC”) is the world’s largest movie theater operator with more than 850 theaters in 11 countries. Chances are we have all been to see a movie at an AMC operated theater in the U.S. AMC was formed in 1920 in Kansas City, Missouri, and its shares are traded on the New York Stock Exchange as “AMC.”

The Legacy Movie Industry (Pre-2000)

Historically, the business model was simple: Hollywood studios would produce a movie and secure distribution through theaters (including AMC) for first run films. Theaters then charge ticket prices to theatergoers. Margins are traditionally thin on movie tickets, but AMC and other theater operators could count on concession sales to boost profitability.

Over the last 25 years, movie goers became gradually and then suddenly less interested in seeing movies in theaters. According to Pew Research, U.S. (and Canadian) ticket sales peaked in the early 2000s with annual sales above 1.5 billion tickets between 2001 and 2003. That number gradually fell to under 1.3 billion tickets by 2010. Ticket sales then stayed generally above 1.2 billion tickets between 2010 and 2020, but there was a modest downward trend over the decade.

When the pandemic hit in early 2020, and theater ticket sales plummeted to just 230 million tickets. Today, sales still have not recovered to pre-pandemic levels. Research from Pew suggests that about 770 million tickets were sold domestically in 2025. Throw in a few strikes, which delayed projects, and the movie-going public’s fatigue around certain franchises, and you have a recipe for trouble for legacy movie distribution channels.

The Rise of Streaming (Post-2000)

The rise of streaming platforms like Netflix, Amazon Prime, Hulu, and others has discouraged audiences from going to the theater for two reasons. First, streaming platforms have in-house production studios which only release certain movies and shows on their platforms, and not necessarily in the theaters. Second, post-pandemic, viewers prefer the comfort of their own living rooms to going out to the theater. For a deeper dive into streaming powerhouse Netflix, read TRA’s Expanded Report.

AMC and other theater operators have always been middlemen, beholden to move product between a seller (the movie studios) and a buyer (the movie-going public). Movie studios pay for and produce content, and then secure a certain number of screens both in and outside the U.S. at a point in the year where studio and its producers feel a film has the best chance at being economically or critically successful. Moviegoers either accept these films and pay for tickets or opt out on the theater experience. The theater operators have limited ability to influence the types of projects coming out of Hollywood studios.

AMC, Today

AMC has never had strong credit. Even before the pandemic, AMC had poor credit due to the high degree of leverage. Movie theaters are expensive to build and operate, which usually includes high rent and high maintenance costs. For example, in 2019, before the pandemic, AMC had a highly speculative credit rating of B (S&P and Fitch) and B2 (Moody’s). AMC had acquired Carmike in 2016 and was already navigating the troubled cinema landscape.

Fast forward through the pandemic, after a brief period with meme stock status, AMC turned to a new strategy to stave off its decline. The company, which is highly leveraged with more than $4 billion in borrowings, started its liability management exercise, which is a fancy way of saying the company is negotiating with creditors and attempting to trade assets or equity to keep the lights on. AMC’s management team has pledged to not raise any more capital through equity issuances. This avoids dilution of existing equity holders and allows them to focus on expense reduction and may help prevent further credit weakness. Today, AMC (at least the restricted portion) has credit ratings on its debt that are extremely speculative or suggestive of imminent default of CCC- (S&P) and Caa2 (Moody’s).

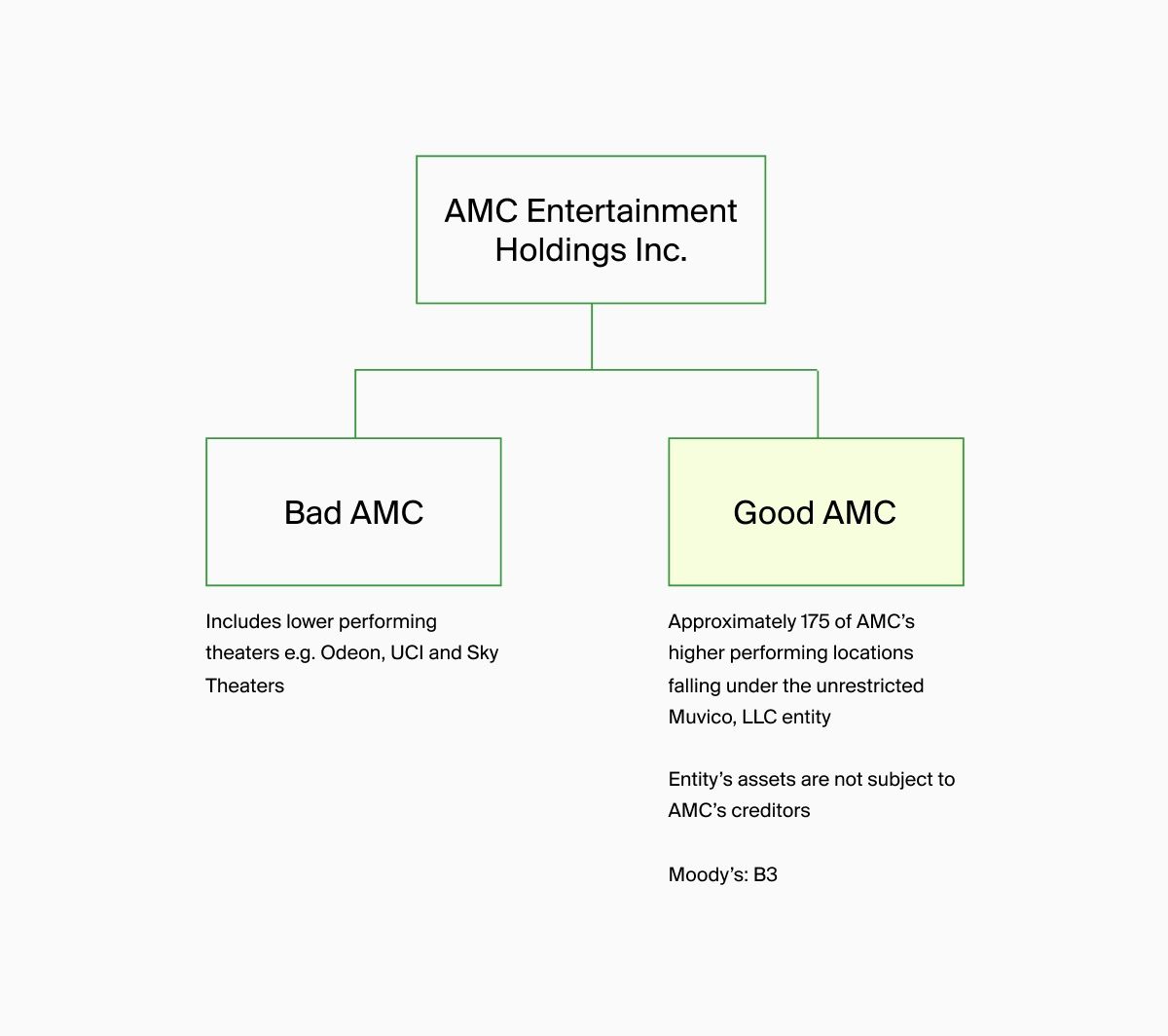

A New Structure: the “Good AMC” and the “Bad AMC”

There are now essentially two AMC entities, which we can be simplified into the“Good AMC” and the “Bad AMC.” A new entity was created called Muvico (the “Good AMC”) to hold AMC’s 175 or so best preforming locations. Muvico/the Good AMC holds a little over half of the company’s operating profit. Muvivo sits under another entity called Centertainment, and these two entities and their assets sit outside of AMC’s term loans, with creditors unable to make claims against them.

The ”Bad AMC”, meanwhile, remain under their legacy legal entities and are subject to the term debt. AMC’s plans to date have included closing the low-performing theaters, restructuring leases, or finding other alternatives. AMC has said it no longer plans to sell new shares of AMC Holdings, Inc. to avoid further dilution, but it has completed some distressed exchanges, which gives some creditors equity in exchange for extinguishing a portion of the outstanding debt.

Impact on Landlords

To be clear, there is no very strong AMC entity, but landlords will be better positioned if their tenants consolidated through Muvico, LLC (Good AMC), as those are the profitable locations. Landlords whose assets have a lower performing entity on the lease under Bad AMC could face closure of locations or requests for rent relief. Opting to offer such relief should be considered carefully, or come with credit enhancements from Good AMC.

In the meantime, the industry remains reliant on more blockbuster films and its ongoing ability to work with lenders. This saga is poised to play out over the next five plus years.